Myths About Today’s Housing Market [INFOGRAPHIC]

kcm • May 6, 2022

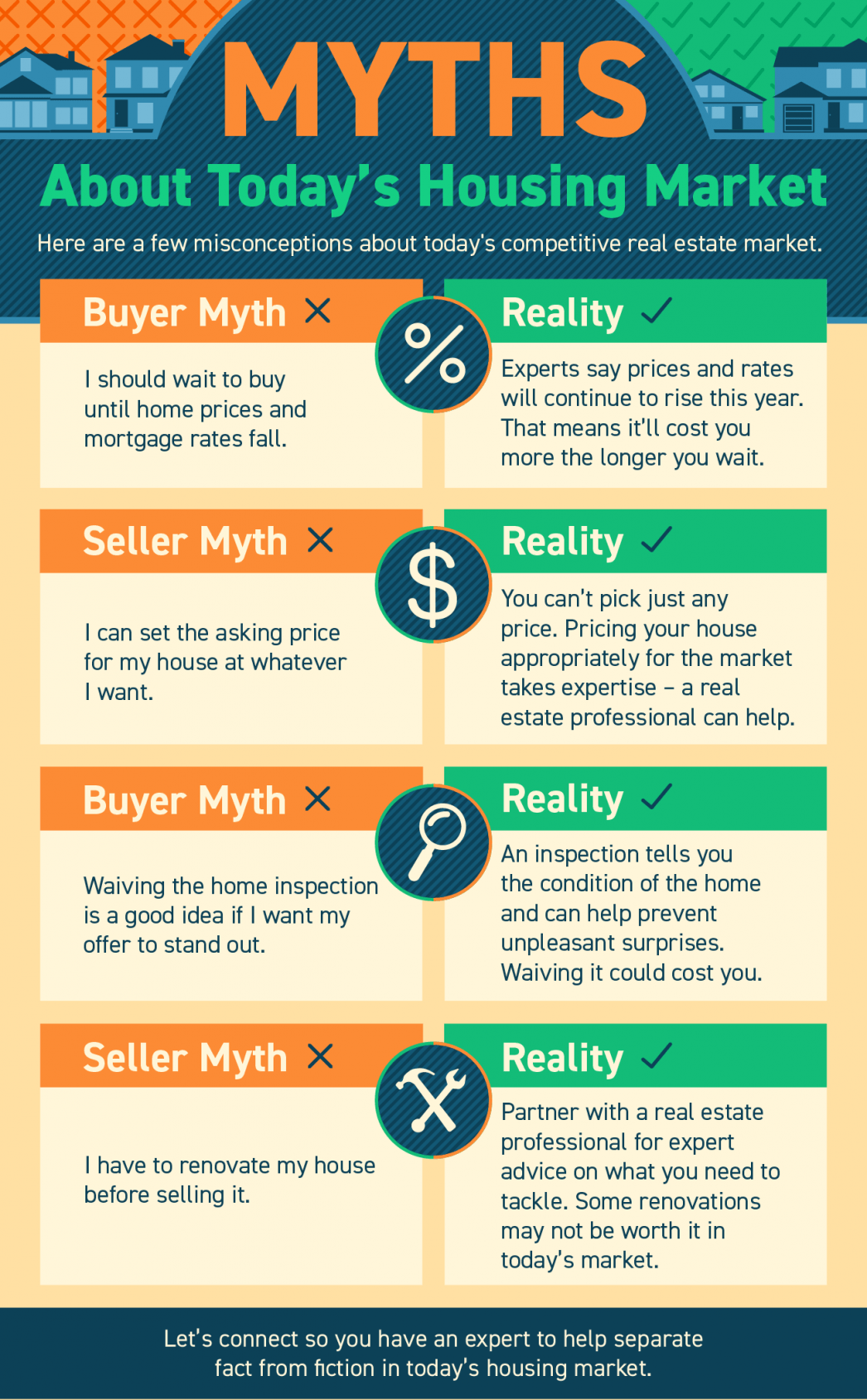

Myths About Today’s Housing Market [INFOGRAPHIC]

Some Highlights

- If you’re planning to buy or sell a home today, it’s important to be aware of common misconceptions.

- Whether it’s timing your purchase as a buyer based on home prices and mortgage rates or knowing what to upgrade or repair before listing your house as a seller, it takes a professional to guide you through those decisions.

- Let’s connect so you have an expert to help separate fact from fiction in today’s housing market.

Share this post

Housing affordability has become one of those rare topics almost everyone agrees on: it’s a problem. Buyers feel it, renters feel it even more, homeowners talk about it, and politicians on both sides of the aisle regularly float ideas on how to fix it. Tax credits, zoning changes, interest rate adjustments, down payment assistance programs — for nearly every proposed solution, there’s a counterargument about whether it actually helps or just sounds good on paper. But one idea comes up again and again, across government, finance, real estate, and even everyday conversations among buyers and homeowners: build more homes. At its core, real estate is supply and demand in action. When demand outpaces supply, prices rise. When supply catches up, prices tend to stabilize or fall. So the logic is simple enough. If affordability is the issue, adding more housing inventory should help relieve some of the pressure. Of course, that doesn’t mean it’s easy. Builders aren’t public utilities. They’re private businesses with margins to protect, financing costs to manage, and risk to account for. Construction costs, labor shortages, permitting delays, and interest rates all play a role in whether new homes will actually get built. But with enough incentives and pent-up demand, it’s not unreasonable to think we could see a meaningful wave of new construction in the near future. And if that happens, you might just find yourself excited to go out and look for a new construction home! A Lot of Buyers Casually Walk Into a Model Home for a “Quick Look” For many buyers, the new construction process starts casually. Maybe they drive past a new development and decide to pull in. They walk through a model home “just to look.” They chat with the on-site sales representative — or even the builder directly. It feels low-pressure, informational, and harmless. After all, no one’s signing anything… yet. But what often happens next is where things get complicated. Buyers go home and sleep on it. They come back another time. Maybe even a third. Eventually, it starts to feel real — and that’s when many decide it would be smart to bring in their own real estate agent for guidance, negotiation help, and an extra set of eyes on the contract. Unfortunately, when they try to do that, they often find out it’s already too late to get their own agent involved. Why That First Visit Matters More than Most Buyers Realize What many buyers don’t realize is that the very first visit to a new construction site quietly sets the rules for how the rest of the transaction will unfold. From the builder’s perspective, walking into a model home without an agent isn’t just a casual look, it potentially establishes the buyer as someone working directly with the builder’s sales team. Many builders have clear internal policies that say if a buyer’s first interaction happens without a real estate agent present, that buyer is considered “registered” to the builder. Once that happens, bringing in an outside agent later may not be allowed at all, or may require special approval which can be difficult to obtain. Why? Because builders aim to keep tight control over their sales process. They control the product, the pricing, the incentives, the timelines, and the messaging. Introducing an independent buyer’s agent — especially after conversations, tours, or pricing discussions have already started — adds another voice to the process. And that voice is focused solely on the buyer’s interests. That doesn’t make builders villains. It’s simply how many new construction sales are structured. But it does mean that a decision that feels small in the moment — “Let’s just stop in and take a look” — can have lasting consequences. By the time buyers realize they want professional representation and negotiation help, the window to involve their own agent may already be closed. “Do I Even Need My Own Agent for New Construction?” Some buyers, especially those who like the idea of a streamlined process, question whether bringing their own agent makes sense at all. After all, the builder already has a sales rep. The price is often set. The home is brand new. What’s there to negotiate? It’s a fair question — and one that builders are happy to let buyers ask themselves. But it’s important to remember that the builder’s sales agent works for the builder. Their job is to protect the builder’s timeline, pricing, and contract terms. They are not obligated to point out unfavorable clauses, suggest alternatives, or flag long-term resale considerations. An independent buyer’s agent serves a very different role. Their responsibility is to the buyer — not the builder. That means advising on contract terms, explaining how builder add-ons and incentives actually affect the bottom line, and helping buyers understand where there may be room to negotiate, even when the base price appears “fixed.” In new construction, negotiations often happen in less obvious places. Closing cost credits, upgrade packages, lot premiums, build timelines, contingency language, and even how issues are handled during construction can all have real financial and practical implications. These are details buyers may not think to question, but they can matter long after the excitement of choosing finishes wears off. An experienced agent can also provide context that isn’t available in the model home. How this builder compares to others nearby. How resale values have held up in similar developments. Whether certain upgrades tend to pay off (or not) when it comes time to sell. That kind of perspective doesn’t come from the builder’s sales office, because it doesn’t serve their interests to provide it. In short, new construction may look like a straightforward sales process on the surface, but it’s still a real estate transaction between a buyer and a seller. A seller who is often much more experienced than the buyer… So if you find yourself tempted to stroll into a model home in the near future, it may be worth pausing and scheduling that first visit with your own real estate agent instead. The Takeaway: If new construction inventory starts to increase, that’s good news for buyers and the market as a whole. More options, less pressure, and a healthier balance between supply and demand are all positives. But buyers should slow down before casually walking into a model home alone. If there’s any chance you’ll want an agent to be involved in the purchase, they should be part of the first visit — or at least formally registered in advance. A quick conversation upfront can preserve options, protect representation, and prevent frustration later.

You may have seen the headlines making the rounds lately about a homeowner who supposedly sold his house using AI. At face value, it sounds like something straight out of the near future. Most of the headlines made it seem like the guy typed in a few prompts and AI handled the marketing, found a buyer, guided the negotiations, and just like that… sold. But if you actually listen to an interview with the seller, the story sounds a little different. He makes it clear that AI was more of a tool helping with pricing ideas, marketing, and understanding the general process of selling a house. He also openly admitted that he hired an attorney to review the contract. So, like a lot of things you see online, it wasn’t quite as simple as it was made to sound. And as it turns out… he had even more help than he let on. The Part That’s Not Getting Talked About According to this article from the National Association of Realtors , there’s a key detail that tends to get left out of the story. There was a real estate agent involved. Not representing the seller, but representing the buyer—and in the process, doing a lot more than just “bringing the buyer.” While the seller enlisted the help of an attorney, he still found himself needing timely help and answers. So the agent ended up taking calls from the seller on a daily basis, from as early as 7:30 AM to as late as 11 PM one evening, helping answer his questions and guiding him through the process. In other words, doing many of the things a listing agent typically does, in order to help her client successfully buy a house from a seller who didn’t know the process. The reality is, this wasn’t a case of “AI handled everything.” There were still several humans involved, and one of them was an experienced real estate agent helping navigate the deal. Headlines Should’ve Said: “Local Man Sells House for Sale by Owner” When you really stop and think about it, this really is nothing more than a story about a For Sale By Owner (FSBO) transaction. This is really nothing new. A percentage of homeowners choose to go that route every single year. Some have success. Most quickly realize there’s more to the process than they expected. The only difference here is the tool being used. Not many years ago, this headline might have read: “Homeowner Sells House Using the Internet!” People have used Google to find information, online tools to create marketing for their home, and websites to expose their home to the market. Today, it’s AI. Different technological innovation. Same basic concept. Because at the end of the day, technology can help you get in the game… but it doesn’t suddenly make you an expert in everything that happens once you’re in it. Then Again, FSBOs Are at an All-Time Low… According to the National Association of Realtors , despite all the technology available today, For Sale By Owner transactions are at an all-time low, accounting for just 5% of all home sales. So all of those headlines probably should have focused on the fact that he sold his house FSBO! That’s probably more accurate. At a time when sellers have more access than ever to information, marketing tools, and now AI, the overwhelming majority still choose to work with a real estate agent. That doesn’t mean technology isn’t helpful. It is. AI can give you ideas, help you understand the process, and even make you feel more confident getting started if you’re thinking about selling on your own. But there’s a big difference between having access to tools, and knowing how to navigate everything that happens once your home hits the market. Pricing strategy. Buyer psychology. Negotiations. Inspections. Appraisals. Timelines. The unexpected issues that almost always come up along the way. That’s where experience tends to matter most. So if you’re thinking about using AI to sell your home based on this story, just know there’s more to it than meets the eye—and a reason why most sellers still choose not to go it alone. The Takeaway: A recent viral story about someone selling their house using AI makes it sound like the future has officially arrived. The headlines make it seem like all you have to do is type a few prompts, sit back, and watch your house sell. In reality, AI helped with some of the early steps, but there were still plenty of humans involved—including a buyer’s agent who ended up fielding calls and walking the seller through much of the process. So what you’re hearing about wasn’t a fully automated home sale. It was a For Sale By Owner deal with some tech mixed in. And considering FSBOs are at an all-time low of just 5%, that’s probably the part that should have made the headlines.

It’s common to look around your current home and wish for something better. More space. A different layout. A better location. Fewer compromises. That feeling doesn’t mean there’s anything wrong with your home—or with you. Very few people live in a place that feels perfect forever, and it’s human nature to wonder whether a different home might make you happier. That’s why a recent article from Realtor.com about whether a new home can make you happier can feel a little…conflicting. On one hand, it suggests that buying a new home could increase happiness. On the other hand, it says it might not. It’s an honest take, but it doesn’t really help much. The reality is, there’s rarely a definitive answer. True happiness usually runs deeper than square footage, finishes, or a new address. But if you’re hoping for some real clarity about whether buying a new home will actually make you happier, there may be a place to look for answers that most people don’t initially think to turn to… Most People Start by Venting to Friends, family…and ChatGPT When people start wondering whether a new home would actually make them happier, they usually don’t start by talking to a real estate professional. They start by bouncing it off of the people (and tools) they have in their day-to-day lives, such as: Friends , who know your personality, your habits, and the things you’ve been venting about for years Family members , especially if you’re close-knit—or if they’re providing financial help and feel entitled to weigh in A significant other , since any move will likely impact their life (and happiness) as well ChatGPT and other online tools , are increasingly being used to run scenarios, compare options, or talk through pros and cons Even a therapist , where big life decisions like housing naturally come up Each of these can be genuinely helpful—and in many cases, necessary—to make a thoughtful decision. The problem is that taken together, they can also make the decision more confusing than clarifying. Friends and family often filter advice through their own experiences, regrets, or wins Loved ones may unintentionally project fears or expectations that don’t fully apply to your situation Therapists can help you understand how you feel, but not whether a specific home or market reality actually makes sense Technology can explain concepts, but it doesn’t know your local market, what’s truly available, or which trade-offs are realistic All of these perspectives may help you sort through what you think will make you happy. What they tend to lack, however, is true insight into real estate itself. But Very Few Think to Confide in a Real Estate Agent For many buyers, real estate agents are still viewed through a pretty narrow lens. They’re seen as the person who schedules showings, unlocks doors, writes up paperwork, and—if you’re being cynical—tries to get a deal done as quickly as possible. That perception isn’t entirely surprising, since much of an agent’s work happens behind the scenes. But the truth is, good agents bring far more to the table than they’re usually given credit for—and in many cases, more than they’re ever paid for. Of course, they handle the things most people envision: showing houses, marketing listings, negotiations, inspections, managing timelines, contracts, and all the moving pieces that make a transaction actually happen. But those are just the baseline skills. The real value often lies in what agents learn and refine over years of working with people, not just properties. They’ve watched buyers chase homes they thought would make them happier, but didn’t deliver long-term satisfaction. They’ve helped others find unexpected joy in homes they initially overlooked. They’ve seen decisions driven by emotion work out beautifully—and others unravel under the weight of unrealistic expectations. That experience gives them context that no article, algorithm, or well-meaning friend can replicate. Over time, many agents also develop a set of soft skills that rarely get discussed. They often become an unofficial mix of trusted real estate expert, confidant, sounding board, and—at times—something closer to family. Someone their clients turn to for an uncommon blend of personal perspective and professional insight, wrapped into one relationship. The Sooner You Loop in an Agent, the Clearer the Decision Becomes If you find yourself casually saying things like “If only we had a bigger kitchen,” or “I wish this house had a better layout,” or even half-joking with a friend about how much happier you’d be in a different home, it probably doesn’t feel like a moment that calls for looping in a real estate agent. But that’s actually when bringing an agent into the conversation can be most valuable! A good agent can help you sort through those early thoughts before you make an entirely emotional decision to move forward, or do nothing and cope with a feeling of unhappiness. That doesn’t mean your agent should entirely replace the advice of friends and family, but you should definitely consider adding them in as an objective advisor who also understands the emotional side of the conversation. The Takeaway: It’s completely normal to feel like a new home might make you happier—and sometimes, it really does. That’s why most people start by running their thoughts and feelings by trusted friends, family, or their significant other. Those conversations matter and can be genuinely helpful. But many buyers wait to involve a real estate agent until they’ve already made a firm decision to buy, when in reality, looping one in earlier can be far more valuable. A trusted agent can act as a confidant and objective advisor, helping you sort through emotions, expectations, and real-world possibilities. That early clarity can make all the difference between a move driven by hope alone and one that truly supports long-term happiness.